Between money printing (aka 'quantitative easing'), and a US investor culture that is geared heavily towards future growth and capital gains and largely ignores the payment of dividends (partly also as a result of differing tax treatments between these returns), corporations in the US have amassed significant stockpiles of cash over recent years.

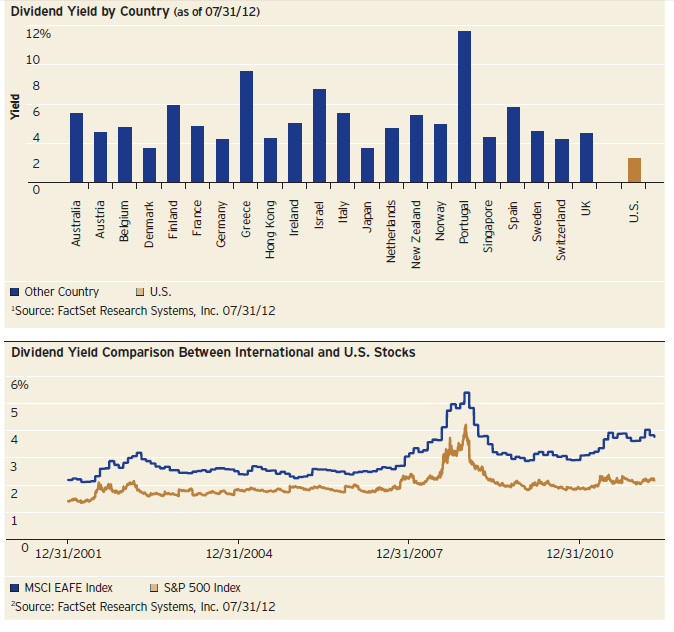

(For a comparison of US to international dividend yields, see these charts: http://static.cdn-seekingalpha.com/uploads/2012/9/16/saupload_Dividend-Yields-by-Country.png, from this article at Seeking Alpha: http://seekingalpha.com/article/869801-u-s-vs-foreign-stocks-a-dividend-yield-comparison)

){kind=link}

Of note, however, is that with interest rates in the US at zero or near-zero levels, the cash sitting on these balance sheets is doing very little to generate a return on assets for shareholders. With these ever-growing stockpiles of cash, generating a negligible return for investors, pressure naturally mounts for this cash to be either (a) returned to investors directly through a special dividend or share buy-back; or (b) used for some productive purpose, which often means growth through acquisition.

Although, to be fair, US interest rates aren't always strictly relevant since huge amounts of cash are not in fact kept in the US at all. See 'Top U.S. Firms Are Cash-Rich Abroad, Cash-Poor at Home' - in fact, some US firms are in the position of having billions of dollars in the bank internationally, but borrowing cash in the US to pay their bills, as the interest rate in the US on those borrowings, is significantly lower than the tax impost of repatriating the cash from overseas!

Well, sort of. To be strictly accurate, the cash *is* often kept in the US, in US bank accounts, invested in US treasuries and the like, but in accounts held by the offshore entities associated with the US firms themselves - see 'Firms Keep Stockpiles of 'Foreign' Cash in U.S.' ...but this discussion isn't about US tax codes and the mechanisms corporations use to manage their cash flow and bank balances, as interesting as these machinations are.

With their famous cash balance of some $137BN, Apple has certainly been subject to a significant amount of this scrutiny (eg http://mobile.blogs.wsj.com/cfo/2012/01/25/apple-feels-pressure-to-use-cash/) as has Google (http://www.cfo-insight.com/financing-liquidity/cash-management/google-cfo-pichette-says-we-need-cash-for-acquisitions/), whose CFO has clearly indicated there is no intent to pay a dividend in the foreseeable future, and the cash is being stored for acquisitions. Given Google's acquisition of Motorola Mobility was completed entirely with cash - $12.5BN of it - there is at least evidence to back this up.

For companies who are considering an exit through trade sale, this trend is very relevant. It certainly remains the case that for smaller transactions, a material proportion of the payment for the company is likely to be made through some kind of share-based or earn-out based mechanism, with the intent being to incentivise the vendors (who are often critical to the success of the business) to continue to work hard and ensure the acquired company continues to fire on all cylinders post-acquisition. But for larger transactions, or transactions where the vendor has successfully managed to 'de-risk' it enough by removing themselves from day-to-day operational roles, all-cash transactions are now significantly more common.

Such a trend should be a significant influence on organisations trying to decide whether or not formalising and documenting processes - and even pursuing an ISO 9001 type accreditation to reflect this formality - is worth pursuing. The neater your business, the more likely the exit will be clean, and paid in cash.

Some impressive corporate cash balances, from their most recent financial data, where necessary converted to USD (using rates on 12/03):

Company Name Balance

Accenture $6,641,000,000.00

Boeing $13,650,000,000.00

Cisco $48,720,000,000.00

EMC $6,167,000,000.00

HP $11,300,000,000.00

IBM $11,130,000,000.00

Infosys $4,210,000,000.00

Intel $18,160,000,000.00

Microsoft $63,040,000,000.00

Northrop Grumman $25,220,000,000.00

NTT $16,850,000,000.00

Raytheon $4,044,000,000.00

Telstra $4,056,000,000.00